Why Snowflake’s cost structure matters more than revenue growth

Snowflake’s revenue growth continues to attract attention. A 29 percent year over year increase and strong net revenue retention make the headline numbers look reassuring.

But the latest 10-Q suggests that the real question is not demand. It is whether the company can turn growth into durable operating leverage under its current cost structure.

Growth alone does not guarantee operating leverage

Snowflake’s business scales with customer consumption. That creates upside in strong demand environments, but it also ties revenue growth directly to infrastructure usage.

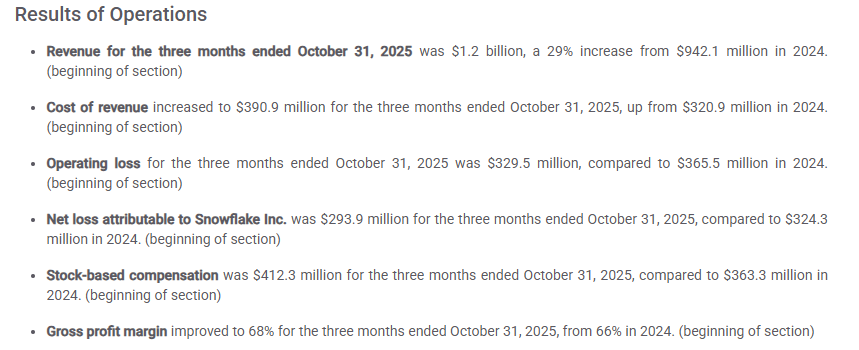

The 10-Q shows that cost of revenue continues to rise alongside revenue. While gross margin improved to 68 percent, operating losses remain significant.

This indicates that scale alone is not yet delivering meaningful margin leverage. Costs are not decoupling from growth.

Cloud infrastructure costs scale with usage

Snowflake relies on third party public cloud infrastructure. As customer workloads grow, infrastructure usage grows with them.

This creates a structural challenge. Unlike software models with near zero marginal cost, Snowflake’s unit economics are closely tied to cloud consumption.

The 10-Q explicitly highlights risks related to cloud disruptions, pricing changes, and performance limitations. These risks translate directly into cost volatility.

Stock based compensation slows the path to profitability

Stock based compensation reached over 400 million dollars for the quarter. This is not a marginal expense.

The filing emphasizes the importance of retaining key personnel and competing for technical talent. In practice, this means equity compensation remains structurally elevated.

As long as stock based compensation stays this high, operating leverage will be harder to achieve even if revenue continues to grow.

Cash trends reinforce the cost discipline question

Cash and cash equivalents declined compared to the start of the fiscal year. At the same time, total liabilities remain elevated and convertible debt remains outstanding.

Snowflake is not facing an immediate liquidity crisis. But declining cash alongside persistent operating losses increases sensitivity to market conditions.

In a tightening environment, cost discipline becomes critical. The 10-Q makes it clear that this transition is still in progress.

The takeaway investors should focus on

Snowflake’s risk is not customer demand. It is execution under a cost structure that scales with usage, talent competition, and cloud economics.

Revenue growth supports the narrative. The 10-Q challenges investors to look beyond it.

Operating leverage is not automatic. It has to be earned.

Read the filing, not just the headlines

This support analysis builds directly on Snowflake’s latest 10-Q and focuses on the cost signals embedded in the document.

If you want to run the same type of risk focused analysis on other companies, you can generate full SEC filing breakdowns inside the StockCompass app.