This balance-sheet risk is hiding behind NVIDIA’s explosive growth

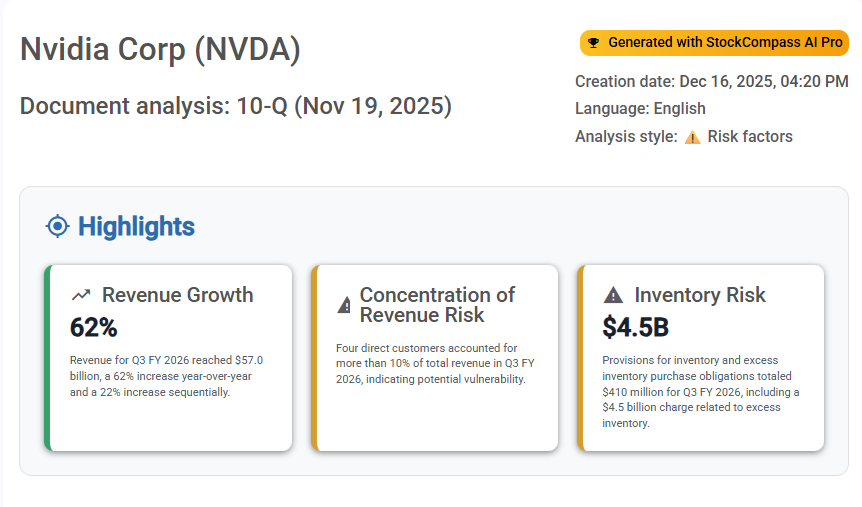

NVIDIA just delivered another quarter of exceptional growth. Revenue is up 62% year over year, operating margins remain extremely high, and demand for AI infrastructure continues to dominate the narrative.

On the surface, everything looks solid. But the latest 10-Q filing reveals a balance-sheet signal that tells a more fragile story beneath the headlines.

Explosive growth, changing balance-sheet dynamics

In Q3 FY 2026, NVIDIA reported revenue of $57.0 billion, driven primarily by Data Center compute and networking platforms. Operating income reached $36.0 billion, and net income for the quarter totaled $31.9 billion.

These numbers explain why market attention remains firmly focused on growth and profitability. However, the balance sheet shows that this growth is becoming increasingly capital-intensive.

Inventories nearly doubled in less than a year

One of the most notable shifts in the filing is inventory. NVIDIA’s inventories increased from $10.1 billion at the beginning of fiscal year 2026 to $19.8 billion as of October 26, 2025.

This represents a near doubling of inventory levels in a period where revenue growth remained exceptionally strong. While inventory build-ups are not unusual during rapid expansion phases, the scale and speed of this increase materially change the company’s working-capital profile.

A $4.5 billion inventory charge already impacted margins

The filing also discloses significant provisions related to inventory and purchase obligations. For the first nine months of fiscal year 2026, inventory and excess inventory purchase obligation charges totaled $6.7 billion, including a $4.5 billion charge associated with excess inventory.

These provisions have already had a measurable effect on profitability. According to the filing, inventory-related charges negatively impacted gross margin by 3.7% year-to-date.

Even with gross margins still reported at an exceptional 73.4% for the quarter, this highlights how quickly balance-sheet pressure can surface when execution timing shifts.

Why this risk is easy to miss

None of these signals appear in earnings headlines. Revenue growth, operating margins, and net income all point in the same positive direction, which naturally dominates investor attention.

Inventory levels, purchase obligations, and working-capital dynamics require deliberate balance-sheet analysis — and they rarely feature in summary commentary.

As long as demand remains strong and execution stays perfectly aligned, these dynamics remain manageable. The risk emerges when growth slows, product transitions accelerate, or customer purchasing behavior shifts unexpectedly.

This is where pressure shows first if conditions change

The latest 10-Q does not suggest immediate financial distress. NVIDIA maintains strong liquidity, with over $60.6 billion in cash, cash equivalents, and marketable securities as of October 26, 2025.

However, the balance sheet makes one thing clear: inventory and working-capital management have become critical execution variables. If growth moderates or timing assumptions break, this is where pressure would surface before it appears in earnings.

Why balance-sheet analysis matters

Risks like these do not invalidate the growth narrative. They add context to it.

This type of signal lives inside the filing itself — not in press releases, earnings calls, or headline summaries. Identifying it consistently requires structured analysis of balance-sheet movements, not just income-statement performance.