Snowflake’s Growth Is Real. The 10-Q Shows Where the Cost Risk Sits.

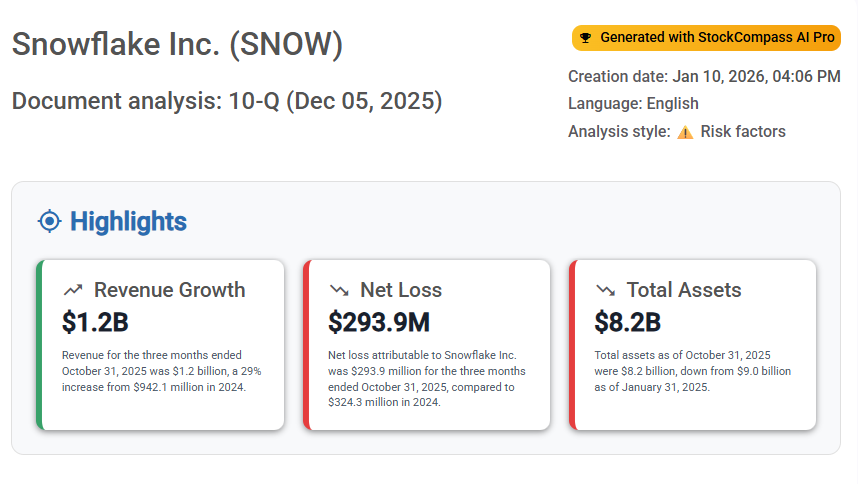

Snowflake continues to report solid top line growth. For the three months ended October 31, 2025, revenue reached $1.2 billion, up from $942.1 million in the same period of 2024. Net revenue retention rate was 125%, and customers with trailing 12 month product revenue greater than $1 million increased to 688 from 534.

On the surface, the growth narrative still looks intact.

But the 10-Q highlights a structural tension investors often underestimate. Snowflake is growing, yet profitability remains constrained by two persistent forces: dependency on public cloud infrastructure costs and heavy stock based compensation.

Revenue growth is strong, but losses persist

Snowflake reported a net loss attributable to Snowflake Inc. of $293.9 million for the quarter, compared to $324.3 million in the prior year. Operating loss was $329.5 million, improving from $365.5 million in 2024.

Cost of revenue increased to $390.9 million, up from $320.9 million a year earlier. Gross profit margin improved to 68% from 66%.

The key point is simple. Growth is real, but the company remains structurally unprofitable at this stage. Margin improvement exists, yet it has not translated into sustained profitability.

Cloud infrastructure dependency limits margin leverage

The 10-Q explicitly highlights the risk of disruptions or outages in public cloud and internet infrastructure, as well as the broader dependence on external cloud platforms.

This matters because Snowflake’s platform runs on third party cloud infrastructure. When your core service depends on public cloud availability and economics, cost control has natural limits. If cloud efficiency does not improve as fast as consumption grows, cost of revenue keeps pressure on margins.

This is not a one time issue. It is a structural feature of a consumption based model operating on third party infrastructure.

Stock based compensation remains a major drag

Stock based compensation was $412.3 million for the quarter, up from $363.3 million in 2024.

The filing also stresses reliance on key personnel and the risk of failing to recruit and retain skilled employees. In practice, this reinforces why equity compensation remains large and persistent.

High stock based compensation is common in growth software companies, but at this level it meaningfully delays the path to durable profitability and increases the importance of operating leverage.

Cash is declining while liabilities remain elevated

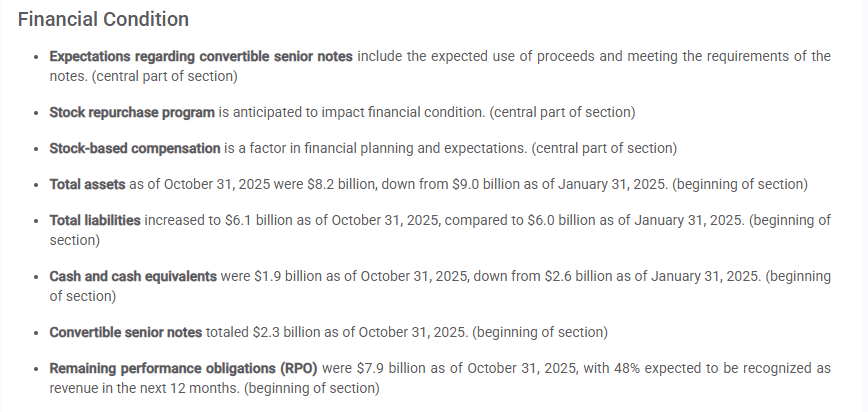

Cash and cash equivalents declined to $1.9 billion as of October 31, 2025, down from $2.6 billion as of January 31, 2025. Total assets declined to $8.2 billion from $9.0 billion over the same period. Total liabilities increased to $6.1 billion from $6.0 billion.

Convertible senior notes totaled $2.3 billion. While liquidity remains meaningful, the direction of cash movement matters. If market conditions tighten, declining cash combined with ongoing operating losses increases execution risk.

The consumption model adds volatility and reduces visibility

The 10-Q highlights limited visibility into future financial position and results of operations due to the consumption based revenue model.

In strong demand environments, consumption accelerates. In slower cycles, consumption can soften quickly. This can pressure revenue timing while cost structure and operational investment remain. That volatility is easy to miss when growth metrics look strong.

The core risk is not demand. It is cost structure discipline.

Snowflake is not struggling with customer interest. The risk is whether the company can translate growth into durable operating leverage while managing cloud driven costs and sustained stock based compensation.

The 10-Q provides the raw signals. Revenue is growing, but net losses persist, stock based compensation remains high, and cash has declined. This combination is the structural risk profile investors should not ignore.

Run the same risk focused filing analysis yourself

This breakdown is based directly on Snowflake’s 10-Q filing and focuses on the risk signals disclosed inside the document. If you want to analyze another company using the same approach, you can generate a risk focused SEC filing analysis in seconds.

Open StockCompass and run a 10-Q risk analysis.

If you want to compare multiple companies side by side, use the same risk analysis style consistently across filings.