Palantir is growing fast, but the risk is still concentrated

Palantir’s latest quarterly results look impressive at first glance. Revenue grew 63% year over year, profitability improved, and margins remain high.

But when you move past the headlines and read the 10-Q carefully, a different picture starts to emerge, one that’s less about growth, and more about dependency risk.

Strong Growth, No Question

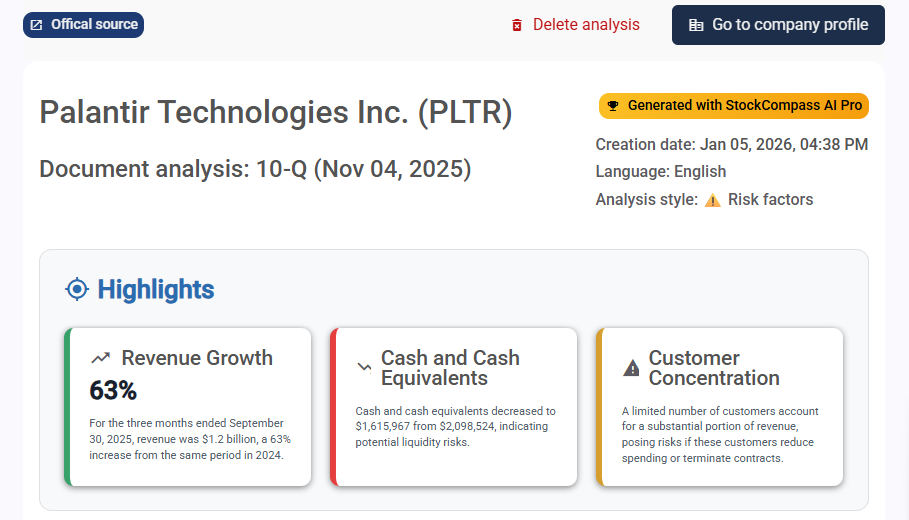

For the three months ended September 30, 2025, Palantir reported revenue of $1.18 billion, up from $725 million a year earlier. Both government and commercial segments contributed to this expansion, with commercial revenue growing faster than government revenue.

Net income also increased sharply, and gross margin reached 82%, reinforcing the idea that Palantir is operating from a position of strength.

On the surface, this looks like a clean growth story.

Where the Risk Starts to Appear

The risk doesn’t sit in revenue growth itself. It sits in who that revenue depends on.

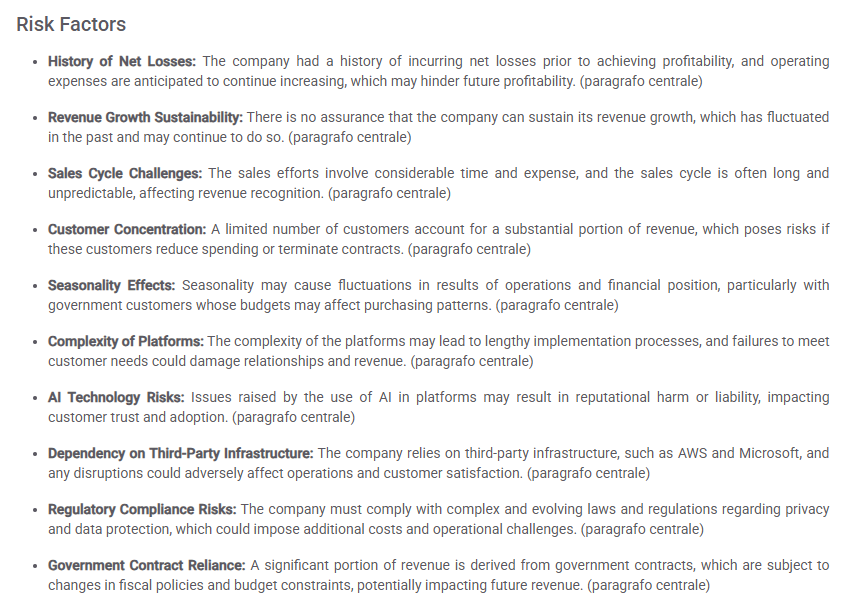

According to the company’s own risk disclosures, a limited number of customers account for a substantial portion of total revenue. This concentration exposes Palantir to meaningful downside if even one major customer reduces spending, delays renewals, or terminates a contract.

This is not a hypothetical scenario. The company explicitly highlights customer concentration as a risk factor in its filings.

Government Dependency Is Still Material

While Palantir has made progress expanding its commercial business, government contracts remain a significant revenue source.

Government customers introduce structural risks that differ from typical enterprise clients:

- Long and unpredictable sales cycles

- Budget-driven purchasing decisions

- Exposure to policy and fiscal changes

Seasonality is also a factor, particularly in government spending patterns. This can create volatility in quarterly results that is unrelated to product demand or execution quality.

Liquidity and Commitments Add Another Layer

Cash and cash equivalents declined to $1.62 billion, down from $2.10 billion at the end of 2024.

At the same time, Palantir has committed to $1.95 billion in cloud hosting obligations over the next decade. These commitments increase fixed costs and reduce flexibility if growth slows or customer behavior changes.

The company also relies heavily on third-party infrastructure providers, introducing operational dependency outside its direct control.

This Isn’t a Bear Case, It’s a Fragility Check

Nothing in the filing suggests Palantir is in trouble today. Revenue is growing, profitability has improved, and liquidity remains sufficient.

But the risk profile is more fragile than the growth narrative suggests. Concentration risk, government dependency, and long-term infrastructure commitments all sit beneath the surface — visible only if you read the filing carefully.

For investors, this shifts the question from:

“Is Palantir growing?”

to:

“How resilient is that growth if a small number of customers change behavior?”

What to Watch Next

- Changes in customer concentration percentages

- Government vs commercial revenue mix over time

- Cash trends relative to long-term commitments

- Any increase in reliance on specific infrastructure providers

These signals won’t appear in headlines — but they will appear in future filings.

Want to Check the Same Risks on Another Company?

This analysis was generated by reading the risk disclosures and financial data directly from Palantir’s 10-Q.

If you want to run the same type of risk-focused analysis on another company, you can do it in seconds.