NVIDIA’s Explosive Q3 FY2026: What the Nov 19, 2025 10-Q Really Shows

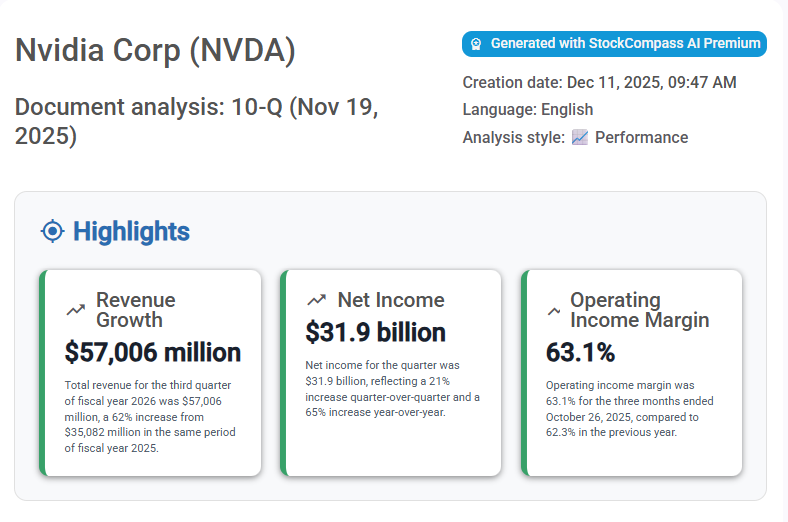

NVIDIA’s November 19, 2025 10-Q filing confirms what the market largely expects but rarely reads in detail: the company is expanding at a scale the semiconductor industry has not seen in decades. With revenue surging to $57,006 million for the quarter, NVIDIA continues to consolidate its position as the central infrastructure provider for global AI deployment.

This article analyzes the filing using StockCompass AI, which automatically extracts every number, percentage, operational detail, and risk factor from SEC filings—saving hours of manual reading.

Try This Analysis on Your Own Filings

Want to analyze any 10-K, 10-Q, or 8-K in seconds?

Select a filing and let StockCompass AI do the reading for you:

1. Revenue Growth Driven Almost Entirely by AI Infrastructure

The quarter’s $57,006 million in revenue represents a 62% year-over-year jump and a 22% sequential increase. Nearly all of this growth originates from the Data Center division, which alone generated:

- $51.2 billion in revenue (up 66% YoY and 25% QoQ)

- Driven by accelerated computing, large-scale AI model deployment, and the continued ramp of Blackwell architectures

Compute revenue grew 56% year-over-year, while networking revenue rose 162% year-over-year, reflecting demand for NVLink and XDR InfiniBand in AI clusters.

Automated Insights Without Reading 200+ Pages

All the figures above come directly from the SEC filing, parsed automatically by StockCompass AI. Instead of manually scanning hundreds of pages, you get clean, structured highlights in seconds.

Let StockCompass read the filings for you →

2. Profitability Expands Alongside Scale

NVIDIA reported:

- Net income: $31.9 billion for the quarter (up 65% year-over-year)

- Operating income: $36,010 million

- Gross margin: 73.4%

- Operating margin: 63.1%

The company remains one of the most profitable enterprises in the world by percentage margin, despite enormous R&D and infrastructure investments. Operating expenses increased 36% year-over-year, yet they still represented only 10.3% of revenue, down from 12.3% the prior year. Scale is doing the heavy lifting.

3. Balance Sheet Strengthens Dramatically

As of October 26, 2025, NVIDIA’s balance sheet looks significantly stronger:

- Total assets: $161,148 million (up from $111,601 million)

- Cash, equivalents, and marketable securities: $60,608 million

- Shareholders’ equity: $118,897 million (up from $79,327 million)

- Inventories: $19,784 million, roughly double the prior level

- Long-term debt: $7,468 million, slightly down

Operating cash flow for the first nine months reached $66,530 million, up from $47,460 million in the prior year period, driven by both volume and margins.

4. Strategic Drivers: The Blackwell Cycle

The filing confirms that NVIDIA’s transition to the Blackwell architecture is now the main revenue engine. Platforms like Blackwell Ultra began shipping earlier in the fiscal year and represent the majority of Data Center demand.

The company highlights:

- Acceleration in AI and agentic applications

- Stronger demand for both compute and networking within Data Center

- Continued ramp of new architectures alongside prior-generation platforms

NVIDIA is no longer just selling GPUs. It is effectively selling AI-scale datacenter blueprints.

5. Risks Hidden in the Footnotes

The 10-Q also surfaces a set of risks that investors should not gloss over:

- Energy and data center capacity constraints could limit or delay AI deployments.

- Export license uncertainty for products like H20 has already resulted in a $4.5 billion charge.

- Customer concentration: a handful of customers account for more than 10% of revenue each.

- Inventory volatility as product transitions accelerate and demand shifts.

These risks are not theoretical. They are already showing up in inventory provisions, regional revenue patterns, and product strategy.

Extract Risk Factors Automatically

Instead of manually hunting for risk factors in dense legal sections, StockCompass AI flags them and summarizes the key points for you.

See risks for your watchlist companies →

6. Capital Returns at Record Levels

Capital return remains aggressive:

- Repurchases of 70 million shares in the quarter

- Repurchases of 262 million shares in the first nine months, for $36.7 billion

- An additional $60.0 billion authorization approved by the Board

- Cash dividends of $732 million year-to-date

This is one of the largest and most sustained buyback programs in the market, funded by exceptional operating cash flow.

7. The Bottom Line: NVIDIA’s Filing Confirms the Strength of the AI Supercycle

The November 19, 2025 10-Q makes three things very clear:

- Demand for AI compute is still accelerating, not plateauing.

- Profitability scales with volume, reinforcing NVIDIA’s competitive moat.

- Regulatory, capacity, and customer-concentration risks are real, but not (yet) enough to derail growth.

For investors, the filing confirms that NVIDIA is not simply riding a hype wave. It is deeply embedded in the infrastructure layer of AI, with numbers that justify the narrative.

Get This Level of Insight on Any SEC Filing

StockCompass AI analyzes 10-K, 10-Q, 8-K and more, extracting key metrics, risks, cash flow dynamics, and segment performance in seconds.

Start for free, no credit card required. One analysis token is included so you can test it on the company you care about most.