Meta’s 10-Q shows the real risk behind the AI and advertising rebound

Meta is often described as a company that “figured it out again”. Advertising is growing, margins recovered, AI is everywhere in earnings calls.

But the 10-Q tells a more complex story.

Behind strong top line growth, Meta is committing to a cost and regulatory structure that materially increases long term risk. This post breaks down where those risks actually sit, using only what Meta itself discloses.

Advertising is growing, but under structural pressure

Meta’s revenue growth is still overwhelmingly advertising driven. Ad impressions are up, pricing improved, and ARPP increased year over year.

The problem is not demand today. The problem is how fragile ad monetization has become.

Privacy regulation, operating system changes, and consent based advertising models in Europe continue to reduce signal quality. Meta openly admits that measurement accuracy is deteriorating and that ad performance is becoming harder to quantify.

This is not cyclical risk. It is structural.

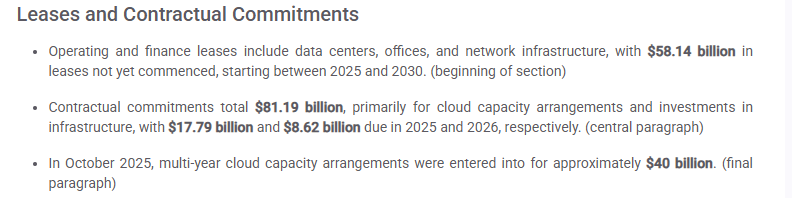

Capex and infrastructure commitments are exploding

Meta is investing at a scale that changes its risk profile.

Capital expenditures for 2025 are guided between $70B and $72B, with further growth expected. Lease commitments, cloud capacity contracts, and data center obligations exceed $80B.

This is not optional spending. Once locked in, these costs are fixed regardless of ad demand volatility.

Meta is effectively trading flexibility for long term AI positioning.

Reality Labs remains a controlled loss machine

Reality Labs continues to lose billions every quarter. Management frames this as long term optionality. The filing frames it as an ongoing drag on operating profit.

Losses have not stabilized meaningfully. Revenue growth in Reality Labs is real, but nowhere near the level required to offset costs.

This matters because AI and metaverse investments are competing for the same capital pool.

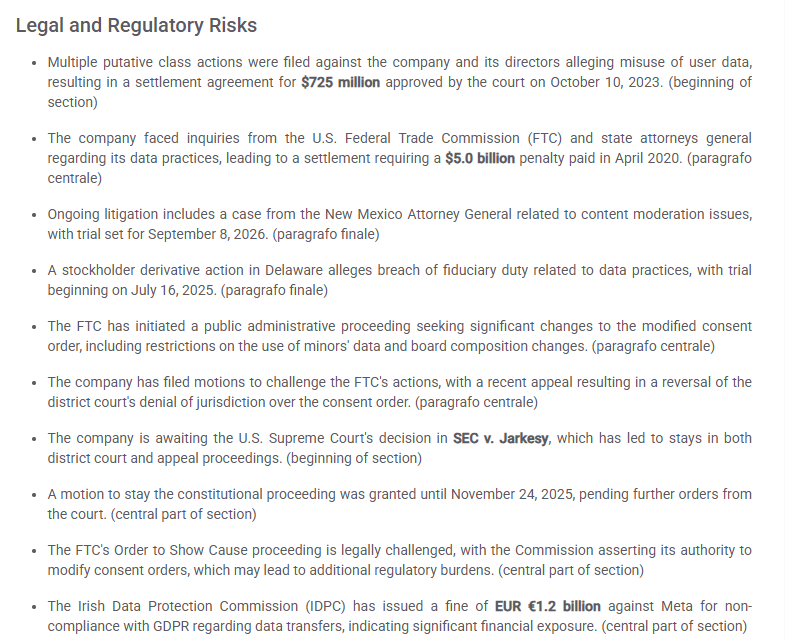

Regulatory and legal exposure is not abstract anymore

Meta’s regulatory risk is no longer theoretical.

The filing documents persistent pressure from regulators and courts, including actions that could materially change data usage, major privacy disputes in Europe, youth related litigation, and antitrust scrutiny.

These are not one off events. They are persistent balance sheet risks.

Financial strength exists, but volatility is increasing

Meta still generates enormous operating cash flow. Liquidity is strong.

However, the filing shows rising earnings volatility, heavy cash outflows for capex and buybacks, and tax related swings that reduce predictability.

This is the tradeoff. Meta is financially strong, but less predictable.

Final takeaway

Meta is not a broken company. But it is no longer a low risk compounder.

The 10-Q shows a business shifting from operating leverage to capital intensity, from regulatory tolerance to regulatory friction, and from clean monetization to measurement uncertainty.

Understanding Meta today means understanding risk first, not growth narratives.

Want to see the full 10-Q risk breakdown, key metrics, and the financial structure without reading hundreds of pages? Explore the complete Meta analysis on StockCompass.