Inside Microsoft’s 10-Q: When AI Scale Starts to Pressure Cash and Flexibility

Document analyzed: Microsoft Corp (MSFT) — Form 10-Q filed Jan 28, 2026.

Analysis style: Risk factors. Generated with StockCompass AI Pro.

Microsoft’s latest 10-Q confirms what the market already knows: revenue and earnings remain strong. The filing, however, highlights a less discussed constraint: cash flexibility under accelerating AI and cloud investment.

This is not a short-term liquidity issue. It is a structural tension between growth ambitions, capital intensity, and capital returns.

Why earnings strength doesn’t guarantee flexibility

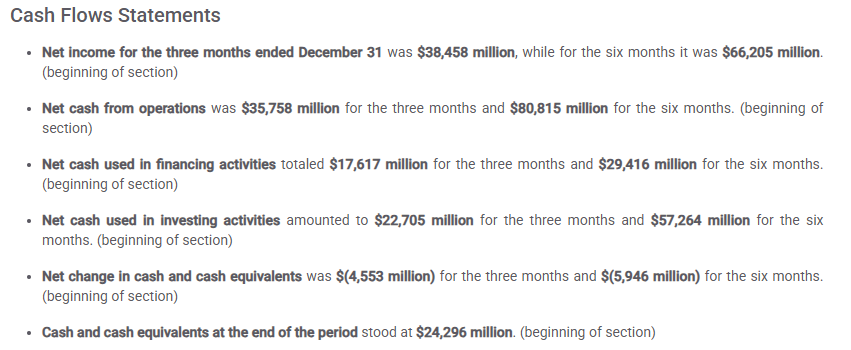

The filing shows robust operating cash generation. At the same time, Microsoft is deploying substantial capital across investing and financing activities.

Capital expenditures for cloud infrastructure, combined with shareholder returns through buybacks and dividends, compete for the same liquidity pool. The result is a declining cash balance despite record profitability.

AI scale introduces execution and margin risk

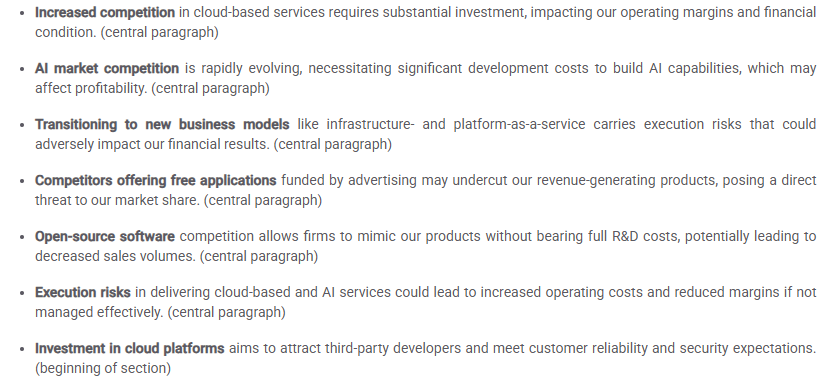

Microsoft’s risk disclosures emphasize that competition in cloud and AI markets requires sustained investment. These investments are speculative by nature and may take time to translate into durable margins.

Execution risk matters here. Large-scale AI deployments raise costs in infrastructure, security, and compliance before operating leverage fully materializes.

The structural takeaway

Microsoft’s risk is not about demand or relevance. It is about how quickly capital intensity rises relative to flexibility.

As AI and cloud scale, cash allocation decisions become more constrained. Monitoring this balance matters more than headline growth.

Extracted in seconds

Identifying these dynamics requires reading across cash flows, risk factors, and capital allocation disclosures. This risk-focused analysis was generated in minutes using StockCompass.

Analyze a 10-Q with StockCompass

Disclaimer: This content is for informational purposes only and does not constitute investment advice.