Amazon’s 10-K: When Scale Becomes Exposure

Document analyzed: Amazon.com, Inc. (AMZN) — Form 10-K filed Feb 06, 2026.

Analysis style: Risk factors. Generated with StockCompass AI Pro in 49 seconds (creation date: Feb 21, 2026).

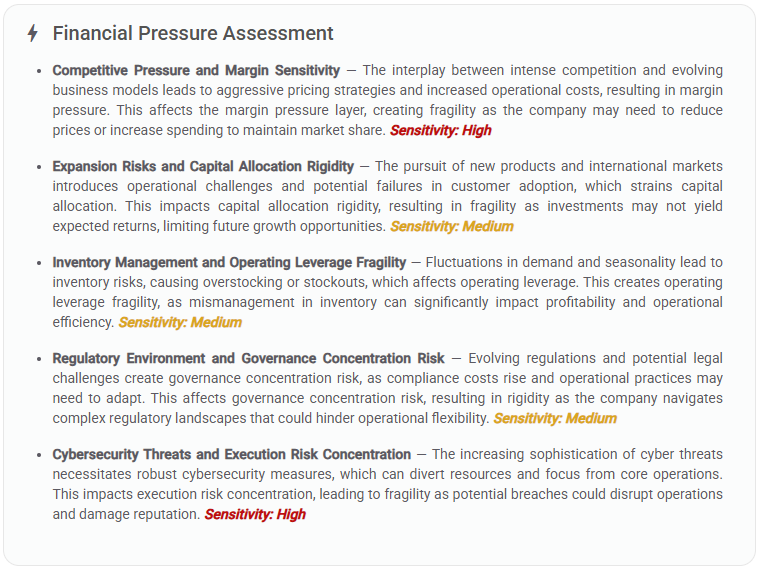

Amazon’s story is usually told as a moat narrative: logistics scale, Prime lock-in, AWS profitability, and relentless execution. The latest 10-K still supports the strength of that machine — but the risk framing is clearer than the hype framing: Amazon’s scale is also a multi-layer exposure surface.

The structural tension isn’t “will Amazon grow?” It’s whether the company can keep expanding while controlling margin sensitivity, capital allocation rigidity, and execution concentration — across retail, services, and infrastructure.

Want the full analysis experience?

Try StockCompass: https://stockcompass.io — see SEC filings distilled into structured risk and pressure signals in under a minute.

View plans

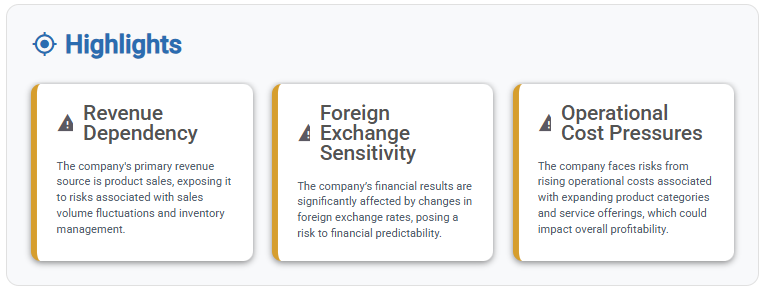

1) Revenue Dependency: A Bigger Engine, a Bigger Sensitivity

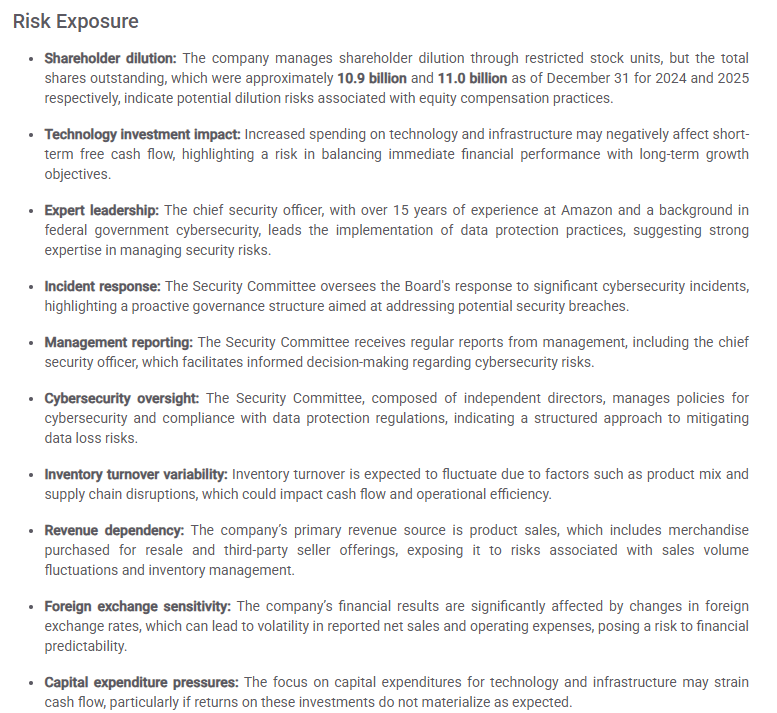

One of the cleanest signals in this risk read is that Amazon’s primary revenue base remains tied to product sales (including first-party sales and third-party seller activity). That breadth is a strength — but it also means volume swings, mix shifts, and inventory dynamics can leak into reported performance faster than investors expect.

In practice: when demand shifts, Amazon doesn’t only face “sales risk.” It faces downstream knock-ons in inventory turnover variability, fulfillment utilization, and unit economics. This is how a diversified catalog can turn into an operational sensitivity layer.

2) Foreign Exchange: Volatility That Pollutes Predictability

Amazon’s international footprint is a growth driver — and a reporting volatility amplifier. With significant exposure to foreign exchange movement, reported net sales and operating expenses can become noisy, making short-term comparability weaker and planning assumptions more fragile.

This isn’t a “currency trading” thesis. It’s a predictability thesis: the more FX becomes a material swing factor, the more difficult it is to distinguish operating improvement from translation effects.

3) Operational Cost Pressures: The Quiet Tax of Expansion

Amazon continues to expand categories, services, and infrastructure. That expansion is growth, but it’s also cost gravity. The analysis flags a consistent exposure: rising operational costs can compress profitability if efficiency gains don’t outpace complexity.

This matters because Amazon’s competitive posture often requires continuous reinvestment: faster delivery, more selection, better pricing, more content, more devices, more compute. The flywheel works — but the “tax” is persistent cost pressure.

4) Capex and Technology Investment: Flexibility vs. Fixed Commitment

The risk read also surfaces a familiar modern tradeoff: technology and infrastructure investment can pressure short-term free cash flow. That’s not inherently negative — but it introduces a discipline test.

Amazon is effectively making a bet that today’s capacity will be monetized by tomorrow’s demand. The failure mode is not “bad strategy.” It’s timing mismatch: when fixed commitments rise faster than returns materialize, flexibility tightens.

5) Security and Execution Concentration: High Stakes, High Blast Radius

Cybersecurity governance appears structured — dedicated oversight, management reporting, incident response framing. That’s a positive. But the bigger point is structural: as Amazon’s surface area grows, the blast radius of a serious incident grows with it.

At Amazon scale, execution risk becomes concentration risk: a disruption doesn’t stay local. It cascades across customer trust, operations, partners, and regulatory scrutiny.

What the structure implies

StockCompass’ Structural Insight frames Amazon’s situation cleanly:

- Revenue volatility exposure — a diverse mix increases sensitivity to changing market conditions.

- FX risk amplification — international breadth adds volatility to reported performance.

- Dilution dynamics — equity compensation can remain a persistent shareholder perception risk.

- Structural cost pressure — attempting variable cost reduction while raising fixed tech commitments can strain margins if growth slows.

Put simply: Amazon can be strong and still be structurally sensitive. The “risk” here is not existential — it’s fragility under stress. The more the model relies on reinvestment and operational excellence, the more mistakes cost.

Bottom line

This 10-K risk read doesn’t argue that Amazon is weak. It argues something more useful: Amazon’s future performance will be decided by discipline under complexity.

In a stable macro environment, scale looks like a moat. Under volatility, scale becomes an exposure surface — and the key variables become margin sensitivity, capital allocation rigidity, inventory leverage, and execution concentration.

If you want to generate this kind of structured SEC analysis in under a minute:

StockCompass → https://stockcompass.io

Plans: https://stockcompass.io/pricing