Alphabet’s 10-Q Looks Strong. The Hidden Risk Is Rising Obligations

Document analyzed: Alphabet Inc. (GOOGL) — Form 10-Q filed Oct 30, 2025.

Analysis style: Risk factors. Generated with StockCompass AI Pro in 21 seconds.

Alphabet’s headline performance remains impressive. Revenue and income are up, Google Cloud continues to expand, and the market narrative stays anchored to “AI momentum.”

But the 10-Q surfaces a more structural story: obligations are rising (liabilities, debt, leases, and long-duration commitments), while legal and privacy exposure remains a persistent overhang. If the cycle turns or costs rebase higher, that combination can compress flexibility quickly.

The balance-sheet shift the headlines won’t mention

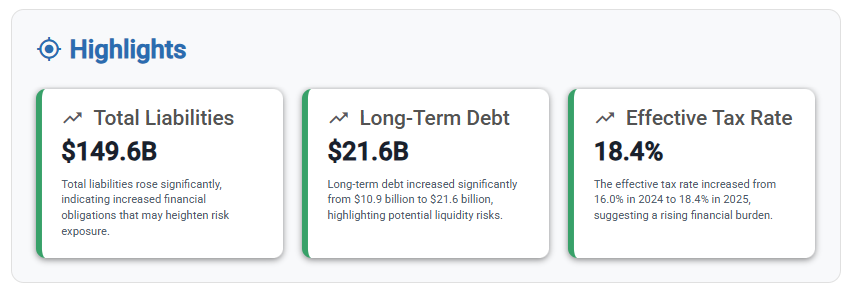

One of the most important signals in this filing is not revenue growth. It’s the direction of obligations. Alphabet’s reported numbers show a clear increase in financial commitments:

- Total liabilities: $149.6B (up materially from the prior year-end period).

- Long-term debt: $21.6B, up from $10.9B — nearly a doubling.

- Lease obligations: future operating lease payments of $17.54B (plus finance leases).

None of this means Alphabet is distressed. It does mean the company is incrementally shifting from “pure flexibility” toward a structure with more embedded commitments — a tradeoff that matters when the operating environment changes.

The real risk: less flexibility in a world of rising constraints

Risk in filings is rarely a single line item. It’s the interaction of constraints: higher obligations plus legal/regulatory friction plus cost pressure. Alphabet’s 10-Q puts all three on the table.

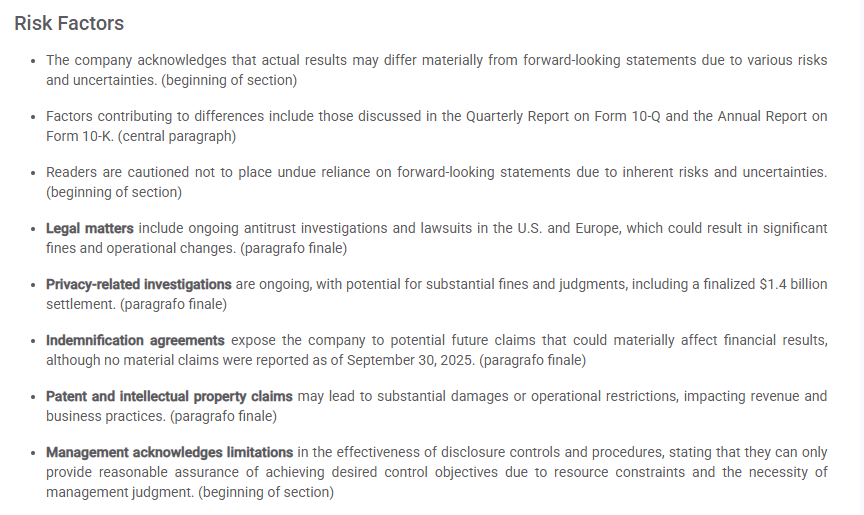

1) Legal and regulatory exposure stays structurally high

Alphabet continues to face ongoing antitrust actions and investigations (U.S. and Europe) that can lead to significant fines and, more importantly, operational changes. The filing also references privacy-related matters, including a finalized $1.4B settlement.

2) Commitments keep compounding (leases, SBC, and long-duration obligations)

Two quieter lines in the filing matter because they represent long-duration cost commitments:

- Stock-based compensation (SBC): $17.9B (nine months), with $47.0B unrecognized compensation cost to be expensed over ~2.6 years.

- Lease costs: up year-over-year (nine months), with meaningful future payment schedules.

SBC is not “free.” It’s a multi-year expense pipeline that can weigh on operating leverage and complicate margin narratives, especially when combined with higher debt and lease commitments.

3) Taxes are trending in the wrong direction

The effective tax rate increased to 18.4% from 16.0%. On its own, that’s not fatal. In combination with other constraints, it’s another pressure point on future profitability.

Cloud: backlog looks strong, but it also creates execution pressure

Alphabet reported a revenue backlog of $157.7B, primarily tied to Google Cloud, with more than 55% expected to be recognized within the next 24 months.

Backlog is good. But it also becomes a forcing function: delivery, infrastructure, and support costs have to execute cleanly while the business continues to absorb higher commitments and legal uncertainty.

The takeaway

Alphabet’s financial performance is strong. The risk is not “Alphabet is broken.” The risk is that obligations are rising (liabilities, debt, leases, SBC pipelines) at the same time the company remains exposed to material legal and privacy outcomes.

In a benign environment, this is manageable. In a tighter environment, it can reduce strategic flexibility faster than most investors expect. That is the structural story hidden behind the headline narrative.

See the raw AI output (and replicate this in minutes)

This risk-focused breakdown took 21 seconds to generate with StockCompass. If you want to extract the same kind of risk structure across companies (without reading filings for hours), use the app and run your own analysis.

Disclaimer: This content is for informational purposes only and does not constitute investment advice.